The Taxpayer Relief Act of 1997 provided homeowners who sell their principal residence an exclusion from capital gains taxes of $250,000 for single filers and $500,000 for joint filers. At that time, the average price of a new home was about $145,000, so this exclusion seemed generous and allowed more Americans to move freely from one home to another.1 Unfortunately, the exclusion was not indexed to inflation, and what seemed generous in 1997 can be restrictive in 2024.

Capital gains taxes apply to the profit from selling a home, so they may be of special concern — and potential surprise — for older homeowners who bought their homes many years ago and might yield well over $500,000 in profits if they sell. In some areas of the country, a home bought for $100,000 in the 1980s could sell for $1 million or more today.2 At a federal tax rate of 15% or 20% (depending on income) plus state taxes in some states, capital gains taxes can take a big bite out of profits when selling a home. Fortunately, there are some things you can do to help reduce the taxes.

Qualifying for exclusion

In order to qualify for the full exclusion, you or your spouse must own the home for at least two years during the five-year period prior to the home sale. You AND your spouse (if filing jointly) must live in the home for at least two years during the same period. The exclusion can only be claimed once every two years. There are a number of exceptions, including rules related to divorce, death, and military service. If you do not qualify for the full exclusion, you may qualify for a partial exclusion if the main reason for the home sale was a change in workplace location, a health issue, or an unforeseeable event.

Increasing basis for lower taxes

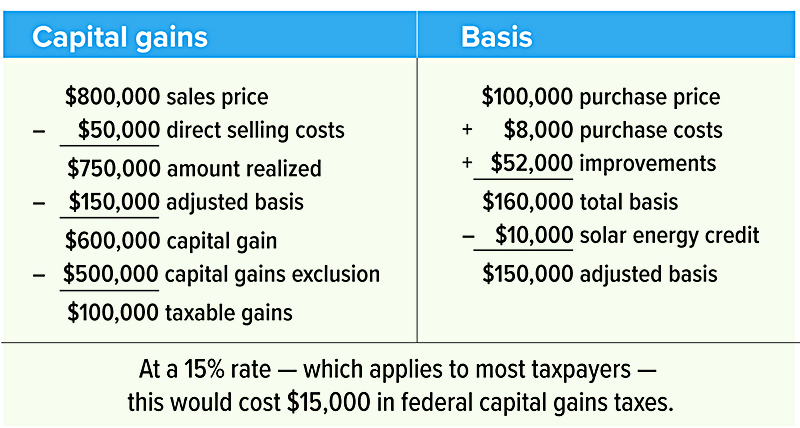

The capital gain (or loss) in selling a home is determined through a two-part calculation. First, the selling price is reduced by direct selling costs, including certain fees and closing costs, real estate commissions, and certain costs that the seller pays for the buyer. (The amount of any mortgage pay-off is not relevant for determining capital gains.) This yields the amount realized, which is then reduced by the adjusted basis.

The basis of your home is the amount you paid for it, including certain costs related to the purchase, plus the costs of improvements that are still part of your home at the date of sale. In general, qualified improvements include new construction or remodeling, such as a room addition or major kitchen remodel, as well as repair-type work that is done as part of a larger project. For example, replacing a broken window would not increase your basis, but replacing the window as part of a project that includes replacing all windows in your house would be eligible. This basis is adjusted by adding certain payments, deductions, and credits such as tax deductions and insurance payments for casualty losses, tax credits for energy improvements, and depreciation for business use of the home. (See hypothetical example.)

Inheriting a home

Upon the death of a homeowner, the basis of the home is stepped up (increased) to the value at the time of death, which means that the heirs will only be liable for future gains. In community property states, this usually also applies to a surviving spouse. In other states, the basis for the surviving spouse is typically increased by half the value at the time of death (i.e., the value of the deceased spouse’s share).

Determining the capital gain on a home sale is complex, so be sure to consult your tax professional. For more information, see IRS Publication 523 Selling Your Home.