U.S. annuity sales set a new record in 2023, due to investor concern with the potential for market volatility and higher interest rates that allowed insurance companies to offer more appealing withdrawal rates. Fixed annuities dominated the market, and about one-third of those sales were for fixed indexed annuities, which can offer growth in a rising stock market while helping to provide protection when the market is falling.1

Of course, the fact that a product is popular doesn’t mean it’s right for you, but it might be worth considering. Indexed annuities are complex, so it’s important to understand how they work and the options you may have if you decide to purchase an indexed annuity contract.

Minimum and indexed returns

Like all annuities, an indexed annuity is a contract with an insurance company that offers an income stream in return for one or more premium payments. Annuity payments may begin right away (immediate annuity) or at a future date (deferred annuity) and are paid over the life of the contract, which might be the owner’s lifetime, the lifetimes of two people, or a specific number of years. Any guarantees are contingent on the financial strength and claims-paying ability of the issuing insurance company.

An indexed annuity usually includes a guaranteed minimum interest rate over the term of the contract — contingent on holding the annuity until the end of the term — typically 1% to 3% of at least 87.5% of the premium. This is combined with a potentially higher rate based on the performance of a specified market index, such as the S&P 500. If index performance is negative, the guaranteed minimum rate will still apply. The indexed rate is calculated in one or more of the following ways.

Participation rate. Determines how much of the index gain will be credited to the annuity. For example, a participation rate of 80% means the annuity would be credited with only 80% of the gain experienced by the index.

Spread/margin/asset fee. May be assessed in addition to, or instead of, a participation rate. For example, if the index gained 10% and the spread/margin/asset fee is 2.5%, then the gain in the annuity would be only 7.5%.

Interest-rate cap. The maximum rate of interest the annuity will earn. For example, if the index gained 10% and the cap rate is 6%, the gain in the annuity would be 6%.

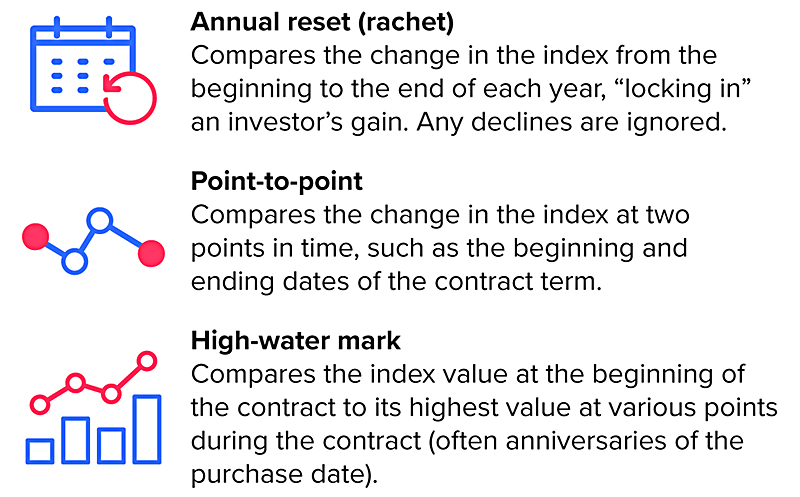

Index performance generally does not include dividends, and the way in which the performance is measured may vary, depending on the contract (see chart). Participation rates, cap rates, and other fees are set by the insurance company, and some companies reserve the right to change these provisions either annually or at the start of each contract term. These types of changes could affect the investment return.

General considerations

Most annuities have surrender charges that are assessed if the contract owner surrenders the annuity during the early years of the contract. However, some indexed annuities allow withdrawals of up to 10% per year without surrender charges. Any withdrawals will reduce the principal, and withdrawals before the end of an index period will receive no interest for that period. Early withdrawals prior to age 59½ may be subject to a 10% federal tax penalty.

Like all annuity contracts, indexed annuities have rules, restrictions, and expenses. Depending on the guarantees of the issuing company, it may be possible to lose money with this type of investment. Be sure to review the contract carefully before deciding whether to invest.

The S&P 500 Index is an unmanaged group of securities that is widely recognized as representative of the U.S. stock market in general. You cannot invest directly in any index, and the performance of an unmanaged index is not indicative of the performance of any specific security. Past performance is not a guarantee of future results.